[et_pb_section fb_built=”1″ admin_label=”section” _builder_version=”3.22″ hover_enabled=”0″ sticky_enabled=”0″][et_pb_row admin_label=”row” _builder_version=”3.25″ background_size=”initial” background_position=”top_left” background_repeat=”repeat” hover_enabled=”0″ sticky_enabled=”0″][et_pb_column type=”4_4″ _builder_version=”3.25″ custom_padding=”|||” custom_padding__hover=”|||”][et_pb_text admin_label=”Text” _builder_version=”4.9.10″ background_size=”initial” background_position=”top_left” background_repeat=”repeat” hover_enabled=”0″ sticky_enabled=”0″]If you run into debt with your tax, you have options, but it is important to do something. Interest charges and penalties accrue from the date the payment is due until full payment is made. If you contact Inland Revenue early and they know you are taking steps to address the debt, they may put a hold on future penalties for late payment which may also be charged. Whereas if you do nothing, interest and penalties can multiply your original tax bill. It is actually possible to double or triple your tax bill, just by hoping it would go away or not knowing what to do about it.

Penalties

If you fail to meet your tax obligations, you are liable for a range of penalties, depending on how serious the default and what kind it is.

For the purposes of late filed returns or overdue tax payments, the kinds of likely penalties are:

▪ late filing penalties

▪ late payment penalties

▪ non-payment penalties

Late filing

The law requires you to file your tax returns by their due dates. If you don’t, you may have to pay a late filing penalty. This penalty is a one-off charge of $50 to $500 per return.

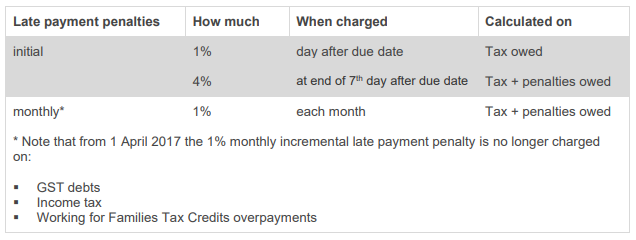

Late payment

As the name suggests, late payment penalties (LPP) come into play if you don’t pay your tax by the due date.

From the table below, you can see how LPP can snowball over time.

Non-payment

Where the non-payment or late payment is in respect of PAYE, Inland Revenue may also charge a non-payment penalty. This penalty is 10% of tax owed and an additional 10% is charged each month up to a total of 15 months (i.e. a 150% penalty).

Interest

Inland Revenue will charge interest on whatever tax and penalties are owing, calculated:

▪ from the date after your tax payment is due

▪ on a daily basis on the amount of underpaid tax, including accumulated penalties and shortfall penalties (however, it does not compound)

The current interest rate is 7.0%.

When you start to pay off a tax debt, Inland Revenue will use the payments to clear any unpaid interest first of all. Provisional tax payments are an exception to this, as you can specify which provisional tax instalment the payment should be used for.

Another exception is that for provisional taxpayers using the standard uplift method, interest will only be payable on the third instalment.

What can I do?

Take action as soon as you can. Contact us to discuss your options to manage the situation.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]

Our specialist tax services are tailored to you, whether you’re a first-time investor or an established, global enterprise. We make sure we take all the stress out of tax compliance and focus on making your business truly tax-effective.

The team we build around your business will work with you on practical, tailored solutions, whether you need to put an entire tax package in place, or just need to know that you’re on the right track.

Property and land transactions

Tax for investors

E-commerce

New immigrants

GST advice and opinions

Foreign investment fund tax

Tax -efficient business structures and development

Using cloud-based accounting services allows businesses to access live financial data anytime from anywhere, and to make faster decisions informed by current information. It improves collaboration with trusted advisors and your internal team. Routine tasks such as bank reconciliation and debtor/creditor management can be automated to free up your valuable time.

Implementation

Training and support for your team to adopt and use software efficiently

We live in a global environment, and many people and businesses have tax obligations beyond New Zealand’s borders. Our work with off-shore clients and our Australian partner firms has earned us specialist expertise in international tax matters that can really benefit you when you need it:

Every business needs to be able to make informed investment decisions with confidence, and to present clear financial data to lenders or investors. Not to mention staying compliant with creditor and tax obligations, and maintaining control over debt and working capital. Forecasting presents a clear picture of these things, and helps to identify pinch-points so that you can address these before they become a problem

All business are different, as are the needs of the business owners. Avoid the pitfalls of cookie-cutter DIY start-up procedures and talk to us by getting your business set up correctly for your unique needs, from day one.

Let us help you to plan for capital requirements, managing cash flow effectively, and staying compliant with IRD and the Companies Office.

Whether you are buying or selling a business, it’s an exciting part of your journey! Preparation and planning is key to a smooth process and we are here to help you.

Advice on preparing your business for sale

Due diligence

Advising on tax-efficient ownership structures

Analysing financial information received for a potential purchase

Providing financial information in regards to a sale

Supporting negotiations

Liaising with brokers and legal and banking professionals

Every year, we’re getting first-hand experience with hundreds of business and their ordinary – and extraordinary – challenges. Whether you’re starting up or broadening your horizons, we have the skills and experience to point you in the best direction.

With that kind of training, our business advisory team are always on hand with innovative and practical solutions that will suit you and your business perfectly.